This glossary pulls together common pharmaceutical terms. Terms range from those used in forecasting, to more general pharmaceutical terms. Simply select the letter from the options, and the correlating terms and definitions will be shown underneath. Please note terms will need to be expanded to show definitions.

Author: user249

Uptake Analyser

Accounting for chronic patients in your forecast

In our latest series of blogs, we’ll be sharing tips and insights gained over the course of our many years of experience.

This post will look at Oncology Forecasting, and accounting for chronic patients in your forecast.

We’ll now hand over to Kris Barker, Senior Consultant here at J+D Forecasting:

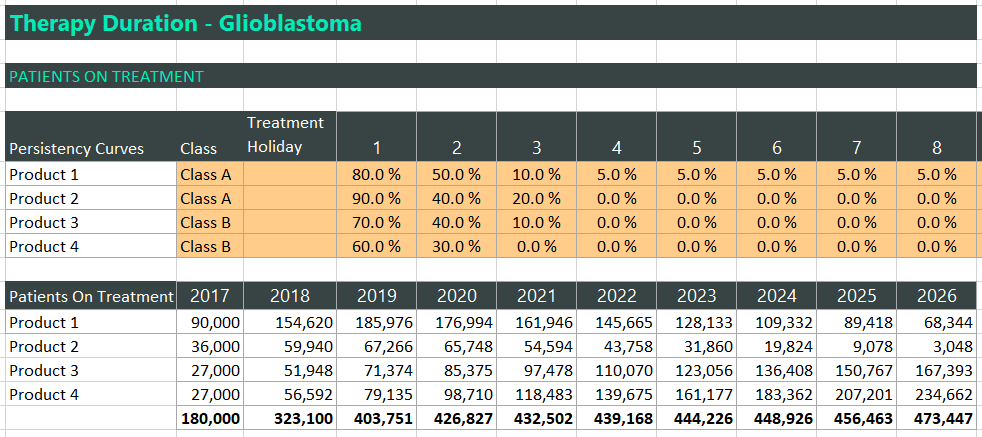

It may well be the case that you have patients who are expected to remain on treatment indefinitely, and hence you need to factor this chronic treatment of patients into your forecast model. With an Onco+ forecast, the easiest way of doing this is to use the ‘persistency curve’ feature within the Therapy Duration section. In this section of your model, you are effectively taking your incident patients at each time period from your Events section, and converting these to ‘patients on treatment’ at each time point using either average length of treatment or persistency curves. Using persistency curves, you can more accurately model the length of time that patients remain on treatment and, if you are needing to model a proportion of patients who receive the treatment indefinitely, then you can make sure that the persistency curve value remains above 0%. In the example below, you can see that for Product 1, there are 5% of all patients treated with this product who remain on this treatment for the duration of the forecast period (whilst all other treatments see the persistency drop to 0%, i.e. no chronic treatment).

Prescriber Universes

Data Sources

Linking an NPV to your sales forecast

In our latest series of blogs, we’ll be sharing tips and insights gained over the course of our many years of experience.

The first three of these will focus on Sales Forecasting, and how linking your forecast to a Profit & Loss account, determining Net Present Value can make for much better evaluation of opportunities.

We’ll now hand over to Kris Barker, Senior Consultant here at J+D Forecasting:

As with many a forecast, the resulting outputs may well be used to drive a go/ no-go decision with regard to progressing the development of as asset or purchasing an asset from another company. To help with this decision, senior management will require more information than just the predicted net sales from your forecast model.

They will need to understand the cost of generating these sales, be it cost of goods, distribution costs, sales force costs etc. And ultimately, they will need to understand the present day value of the future cash stream so that they can compare the opportunity with others that they may be considering at the same time.

As a result, linking your forecast to a profit and loss account that helps you to clearly and consistently present your ‘opportunity’ to senior management is important. This can also be a good way of engaging other colleagues (e.g. finance) into the forecasting process. Ultimately, for the evaluation of a go/ no-go decision, the Net Present Value (NPV) of any opportunity will need to meet the internal requirements of each specific organisation.

In the screen shot below, you can see the calculated NPV for a particular asset. If the internal requirement is that any future opportunity needs to have a positive NPV, then this asset is worth considering. If the internal requirement is that any future opportunity needs to have an NPV of at least $10m, then this asset may not be worth considering.

Feel free to download an example model that links a P&L (including NPV) to the forecast model itself. Please note that linking a P&L to your forecast can be done using any of the FC+ addins.

Glossary

The link above provides you with an NPV Calculator to be used in Microsoft Excel. Here are definitions and more information on some of the terms used in Kristian’s post above.

Net Present Value (NPV)

Net present value (NPV) is the difference between the present value of cash inflows and the present value of cash outflows over a period of time. NPV is used in capital budgeting and investment planning to analyze the profitability of a projected investment or project. Source

Positive Net Present Value

The purpose of net present value is to help analysts and managers decide whether or not new projects are financially viable. Essentially, net present value measures the total amount of gain or loss a project will produce compared to the amount that could be earned simply by saving the money in a bank or investing it in some other opportunity that generates a return equal to the discount rate. If a long-term project has a positive net present value, then it is expected to produce more income than what could be gained by earning the discount rate, which means the company should go ahead with the project. Source

Negative vs Positive Net Present Value

If the net present value of a project or investment, is negative it means the expected rate of return that will be earned on it is less than the discount rate (required rate of return or hurdle rate). This doesn’t necessarily mean the project will “lose money.” It may very well generate accounting profit (net income), but, since the rate of return generated is less than the discount rate, it is considered to destroy value. If the NPV is positive, it creates value. Source

Profit & Loss (P&L) Statement — Formula & Example

The profit & loss statement summarises the revenues and expenses generated by the company over the entire reporting period. The profit & loss statement is also known as the income statement, statement of earnings, statement of operations, or statement of income. The basic equation on which a profit & loss statement is based is Revenues – Expenses = Profit. Source

You might also be interested in our blog – Top 5 Tips for Oncology Forecasting

Trending Example

Trending is one of the key principles that underlay best practice forecasting. Time series trending applies when you have a single data set or one row of data. Briefly, this approach involves plotting historical data against time, and then trending this into the future using an excel generated formula.

We have pulled together an example of how to carry out time series trending within Excel. This can be viewed within the video, or through downloading the related Excel document.

This example aims to walks you through how to trend out historical data within excel, step by step. It will take you through from inputting your historical data, to selecting an appropriate trending curve, and finally to calculating trended data. The example also covers how to convert trend line equations into those recognised by Excel.

If you would like to find out any further information on the principles of trending, the time series trending approach, or other trending methodologies, please visit the training section of theHub or contact us.

How to choose the most appropriate trending approach for a sales forecast

When you are creating a sales-based forecast there can be a wide range of sophisticated forecasting tools available to you.

How do you decide on the best methodology and how do you check the appropriateness? Kris Barker, Senior Consultant at J+D Forecasting discusses:

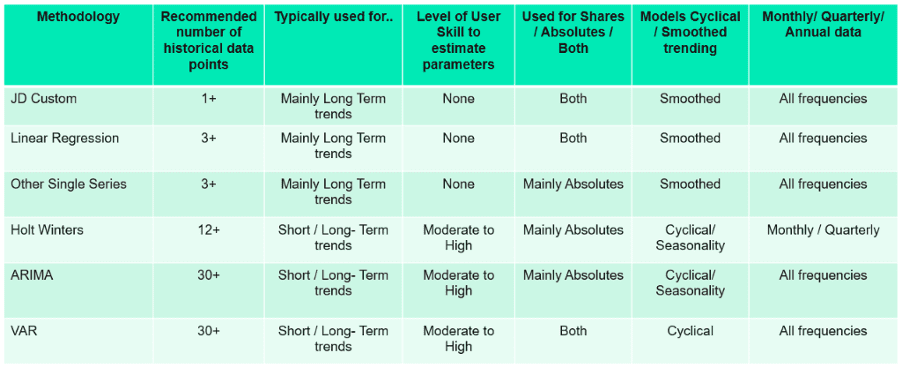

As a starting point, we would recommend using your preferred trending method for all the SKUs/ products/ regimens in your model. This may be a simple growth rate, linear regression, Holt-Winters etc. There are then a couple of checks we would suggest to review the ‘appropriateness’ of your preferred trending option for each product: 1) Review, where applicable, the R-squared value. If this is high, say 60% or above, then you can take comfort in the fact that the trending option selected is doing a reasonable job of using the historic data to predict the future. If this value is low, then this is the first indication that you may want to change your trending option 2) Ultimately, trending algorithms are only mathematical formulas and they cannot think or apply any market understanding that you as the forecaster will possess. As a result, we would certainly recommend reviewing the trending option for any product where the past is not likely to be a very accurate predictor of the future. For example, in cases where a product has only launched in the last 12 months or where a product has had stocking issues over the last 12 months and you know that the volumes are going to ramp up in the coming periods. Trending algorithms are a very quick and easy way of creating your baseline forecast, before you then go on to overlay your events. But they cannot think, and the knowledge and expertise of the forecaster cannot and should not be underestimated when it comes to accurately trending the market in a Sales+ forecast model. But as a general rule of thumb, the screen shot below provides an overview of when each of the different trending options should be considered.

If you’d like some help with building forecasting models or would like to discuss our range of excel based forecasting software please contact us or book a demonstration at a time that suits you.

You might also be interested in Linking an NPV to your sales forecast

Running a risk analysis on consolidated revenues

In our latest series of blogs, we’ll be sharing tips and insights gained over the course of our many years of experience.

This post will look at Epidemiology Forecasting, and running a risk analysis on consolidated revenues.

We’ll now hand over to Kris Barker, Senior Consultant here at J+D Forecasting:

Risk analysis is a very versatile analytical tool available across all the FC+ addins. It may well be the case that you have several forecasts that you have consolidated to create a total, aggregated view of your forecasted revenues. Your next step may then be to create a risk analysis based upon these consolidated revenues and to understand the impact of uncertainty around some of those key variables where your level of knowledge is perhaps not as certain/confident as other input variables. Risk analysis is the perfect tool for this. But to allow you to conduct this analysis on consolidated or aggregated revenues, then there is a very simple additional step required. First of all, the risk analysis section works by selecting input parameters that have a direct or indirect influence on the output variable (e.g. net revenues). Secondly, the output variable needs to a field that is calculated by your forecast model. We need to bear in mind these requirements when conducting our simple additional step. In the example below, you can see that we have created a separate table in our forecast that sums the individual net revenues of the respective countries. As this total net revenue field is a calculated variable, it meets the above requirement. Similarly, as all the input parameters are having an indirect influence on the total net revenue, then this also meets the above requirement. We can now set up and run the risk analysis based on the required input parameters we would like to include and also link this to the total net revenue we have calculated in the simple table we created above. Just click here to take a look at a complete risk analysis we created, which is linked to the above net revenue summary table that you can find on the ‘total net revenue’ tab.

Forecasting by biomarker, not tumour type

If you are forecasting for an asset across multiple tumour types, forecasting using biomarkers may be a favourable approach for you. Especially if you are factoring in multiple countries and scenarios.

How does this work? Kris Barker, senior consultant at J+D Forecasting explains:

Historically, oncology forecasts have often focussed on a specific tumour type as the basis for how the model is structured and populated. If you have an asset that spans across multiple tumour types, this can make forecasting more challenging (especially if you are also factoring in multiple countries and scenarios). In more recent times, the focus has become more on the opportunity for the asset rather than the tumour types for which the asset may get a final indication. It may well be the case that an asset in development targets a specific biomarker across a number of tumour types. BRCA1, as an example, is closely associated with ovarian cancer and to a lesser extent prostate and pancreatic cancer. If you are forecasting an asset that is likely to be closely linked to the BRCA1 biomarker, then it may make more sense to approach your forecast from a biomarker perspective (and to size your potential patient population on those who exhibit this biomarker), than to take an approach based on tumour type.

Download this free example model that demonstrates the above principle.

If you’d like some help with building forecasting models or would like to discuss our range of excel based forecasting software please contact us or book a demonstration at a time that suits you.

You might also be interested in Linking an NPV to your sales forecast